The Payroll Protection Program (PPP) is a form of federal relief that was provided to cash-starved small businesses as a response to the economic troubles caused by the COVID-19 pandemic. When the federal government signed the CARES Act into effect at the end of March of this year, it created two immediate forms of financial relief, the first being the Payroll Protection Program, a loan available to smaller businesses that delivers up to 2.5 times the amount of a business’ monthly payroll. PPP loans can be fully forgiven if spent correctly based on the government’s guidelines: payroll, rent, utilities, and mortgage interest payments.

The second form of financial relief presented came in the expanded form of Economic Injury Disaster Loans, which offer up to $2 million with a fixed low interest rate of 3.75%, coupled with a longer repayment period of up to 10 years. This loan requires collateral if the requested amount exceeds $25,000.

If you’re looking to borrow a small amount of money for your business, Payroll Protection Program Loans are superior in every way—as they always have the potential to be entirely forgiven—whereas Economic Injury Disaster Loans can only be forgiven for up to the first $10,000 borrowed, for the rest of the amount to be repaid over the loan period. For the most part, EID loans are primarily directed toward businesses too large to apply for a PPP loan, which means small businesses that qualify for PPP loans should generally pursue that avenue.

How Truckers Can Make the Most of a PPP Loan

While full forgiveness of a PPP loan is an unbelievably sound financial offer, the drawbacks on spending your PPP loan on something outside of the explicitly approved channels aren’t as bad as you might think. According to information found on the U.S. Small Business Association’s website, PPP loans have an interest rate of only 1%, which is beyond competitive when compared to loans you could have found on the private market.

A large part of driving a semi-truck is managing the up-front costs. For most people starting out in the business, it’s unlikely you’ll get seated in a capable machine without having to find additional financial resources somewhere, somehow. The great thing about trucking is that it doesn’t usually take long to start paying off big chunks of your just-starting-out loans, but it’s always a good idea to prioritize paying off those loans as quickly as you can to avoid paying too much additional interest. For some people, paying off your private loan one year earlier can make a four-figure difference in terms of just how much your rig cost to own outright.

This is where the PPP loan can come to the rescue. If you’re experiencing financial hardship, it can be a strong strategy to take out the largest PPP loan you can be approved for and use that to pay your higher interest-rate debts. This is a form of roundabout refinancing that’s legal under the guidelines for PPP loans, and it’s a practice that private lenders have been encountering and actively encouraging for drivers who have fallen into delinquency on their loans.

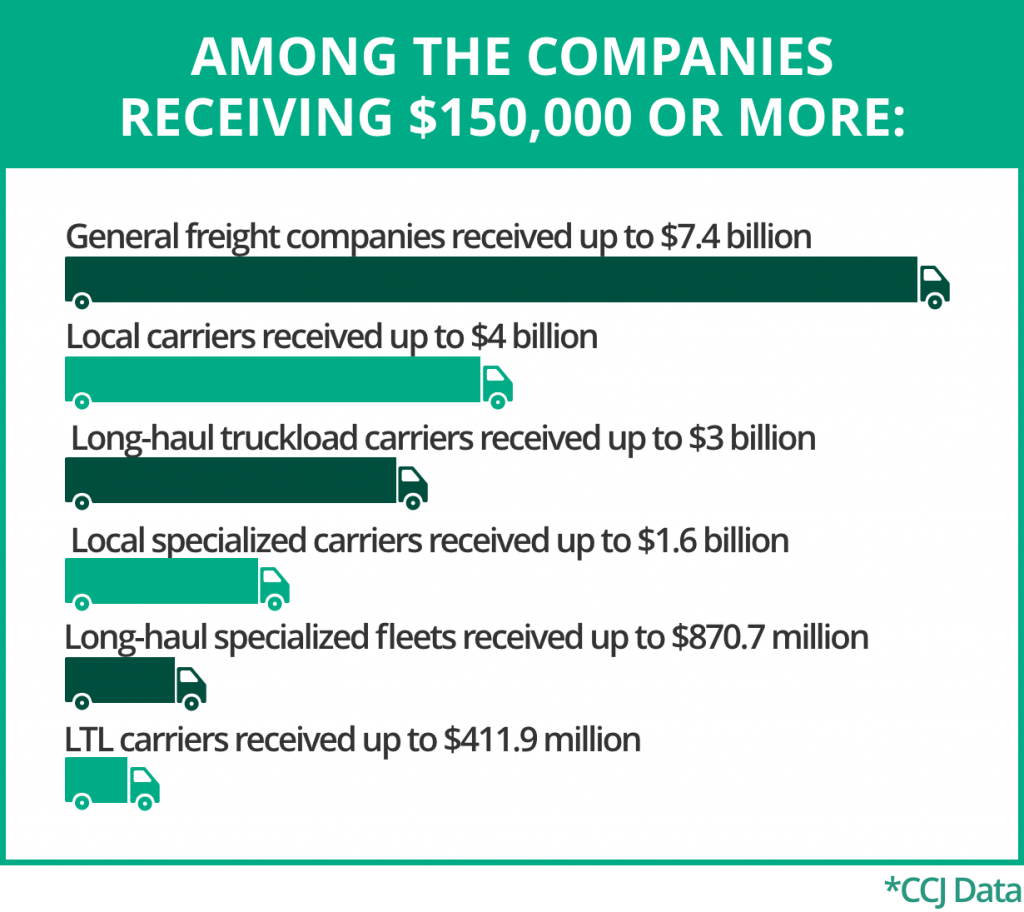

PPP Loans Across the Country

As more than 95% of freight carrier companies in America consist of fewer than five trucks altogether, it makes sense that PPP loans have been a large part of keeping these small businesses afloat during the economic downturn. The Commercial Carrier Journal compiled data on the subject, finding that around 100,000 trucking companies received funds of all sizes, some of which were in excess of $5 million. Local and long-haul trucking companies received $12 billion total, which is more than 2% of all the capital handed out by banks in the United States under the PPP loan program.

In a CCJ survey conducted in June, more than 60% of the fleets that responded said they had applied for PPP funds, with some carriers describing the money as vital for surviving the post-pandemic economic landscape. Another recent survey, conducted by Overdrive, of smaller outfits (independent owner/operators and fleets operating no more than nine trucks), found more than 50% claimed to have applied for PPP loans.

In an interview with CCJ, Mike Kucharski the co-owner and vice president of JKC Trucking, the largest refrigerated trucking fleet in the Chicago Metro area, said his business would have endured layoffs without the more than $2 million loan JKC received through the PPC program. Kucharski said he used the money for payroll, a condition that should allow the loan to be forgiven, but he’s not worried even if things don’t go as expected.

“Even if it doesn’t get forgiven,” Kucharski said, “I think the interest rate they’re going to charge us is a pretty good deal.” Either way, he sees it as a win-win situation.

If you have questions about semi-truck financing, come to the experts. Mission Financial has loan officers well-versed in public and private loan practices who can help you make sense of your next best move.