The freight market is sending mixed signals in May 2026. Volumes are still slightly negative year-over-year. But rates are climbing fast, and capacity is shrinking hard. For owner-operators and small fleet owners, that combination matters a lot.

The Cass Transportation Index is one of the most reliable tools for reading the freight market. It pulls from real freight payment data across thousands of companies and every transportation mode. That means actual spend, not survey predictions. Here’s what the May data tells us, and what it means for your operation right now.

May 2026: The Numbers at a Glance

The three headline figures from May give us a clear market snapshot. They’re important if you’re deciding whether to buy, upgrade, or expand right now.

- The Cass Freight Index for Shipments came in at 1.041. That’s down 1.2% year-over-year but up 3.0% month-over-month.

- The Expenditures Index hit 3.560, up 7.5% year-over-year and 5.3% month-over-month.

- The Truckload Linehaul Index reached 150.8, up 6.9% year-over-year.

In plain terms: fewer shipments than last year, but more money changing hands.

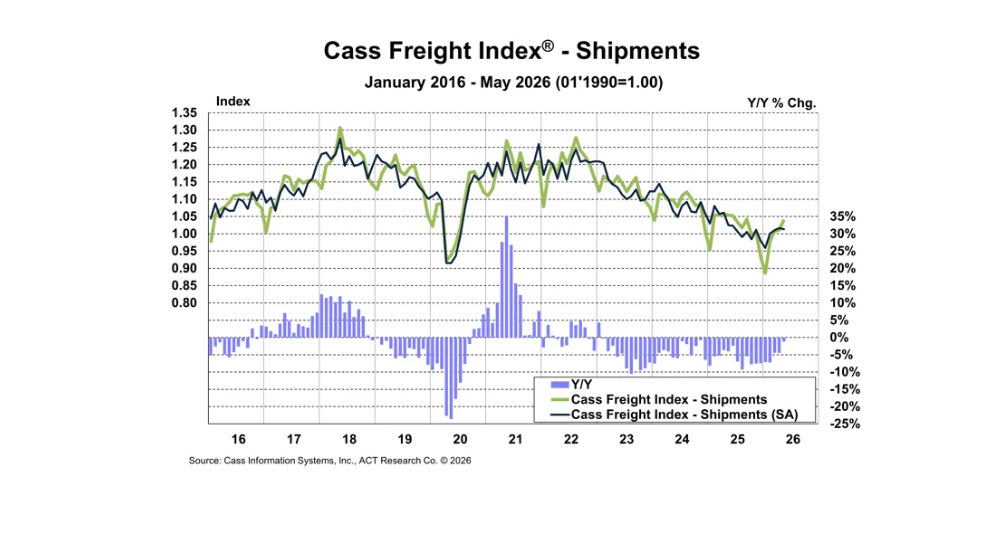

Freight Shipments Are Almost Back in Positive Territory

The year-over-year shipment decline is narrowing fast. At the current trajectory, the market could flip to positive growth sooner than you may think.

The Year-Over-Year Decline Is the Smallest in 18 Months

Shipments came in at 1.041 in May, down 1.2% year-over-year. But that’s the smallest decline in 18 months. After three straight seasonally adjusted monthly gains, the SA reading dipped 0.3% in May. That’s a one-month pause, not a trend reversal. The broader direction is still clearly improving.

Image from cassinfo.com

A Volume Inflection Is Projected for July 2026

At the current run rate, the Cass report projects shipments turning positive year-over-year in July 2026. The domestic intermodal market is already seeing growth. Spot indicators broadly point to improving freight demand. In our experience working with operators through these market cycles, a year-over-year inflection typically shifts negotiating leverage toward carriers. Don’t wait for the numbers to confirm it before you get positioned.

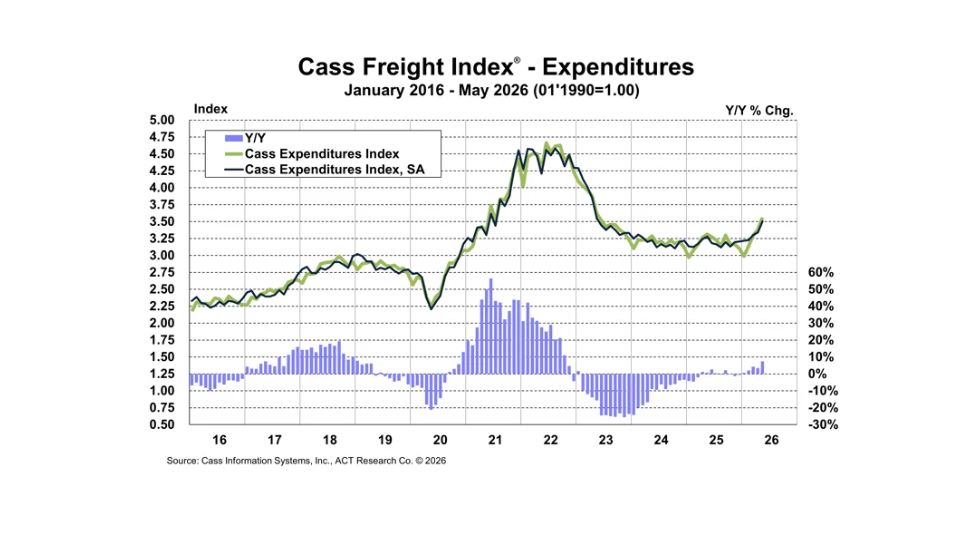

Freight Expenditures Are Surging

While shipments are recovering slowly, the expenditures data tells a very different story. Spending is accelerating at a pace we haven’t seen in years, and it’s picking up speed.

Up 7.5% Year-Over-Year in May

The Expenditures Index hit 3.560 in May, up 7.5% year-over-year. For context, April’s year-over-year gain was only 3.5%. That jump shows how quickly conditions are shifting. In seasonally adjusted terms, expenditures rose 4.9% month-over-month in May alone. Fewer shipment declines plus rising rates equals much higher total spend.

Three Years of Decline Reversed

Freight expenditures fell 19% in 2023, another 11% in 2024, and 0.5% in 2025. That’s three tough years of compressed carrier revenues. The current acceleration is a genuine inflection, not noise. For owner-operators, total revenue potential is growing again after a long stretch of compression.

Image from cassinfo.com

Truckload Linehaul Rates Keep Climbing

Per-mile linehaul rates strip out fuel surcharges and accessorials. That makes the Truckload Linehaul Index one of the cleanest reads on what the market is actually paying per mile. Right now, it’s pointing upward.

The Index Reached 150.8 in May

The Truckload Linehaul Index hit 150.8 in May, up 6.9% year-over-year and 0.4% month-over-month. That figure excludes fuel surcharges and accessorial charges. But both of those are also rising. In the refrigerated market, accessorial charges are climbing, possibly tied to reefer unit fuel costs.

Supply Constraints Are the Real Rate Driver

These rate increases are coming from a capacity crunch. Equipment investment has declined. The ACT Driver Availability Index sits at 32.6, well below the neutral 50 mark. That shows that driver supply is in shortage territory. Rates are expected to keep climbing in the months ahead.

Capacity Is Tightening at a Historic Rate

Here’s what you should pay closest attention to. Available capacity is contracting fast, and the trend isn’t reversing anytime soon.

Six Straight Months of Contraction

The LMI Transportation Capacity Index hit 31.7 in May, up slightly from April’s 28.4 but still at historically low levels. That marks six consecutive months of capacity contraction. Future expectations from the same index point to continued contraction over the next 12 months. Tighter capacity gives carriers with available equipment real negotiating power.

Regulations Are Compounding the Driver Shortage

New Department of Transportation rules on non-domiciled CDLs and English-language proficiency standards have reduced the active driver pool. Combined with reduced equipment investment and ongoing carrier exits, the capacity crunch is building from multiple directions. When fewer trucks are available to take loads, shippers compete harder for capacity, and carriers can charge more.

Diesel Prices: Still Above Year-Ago Levels

Rates are going in your favor. Diesel costs are still a factor, though prices have eased somewhat from earlier this year.

Diesel averaged $4.668 per gallon as of June 29, 2026, according to EIA on-highway diesel fuel price data. That’s still up $0.941 from a year ago. Prices have pulled back from their April highs, which is some relief. But they remain elevated enough to matter for margins, especially on longer hauls.

In our experience, equipment efficiency separates operators who grow in conditions like these from those who just get by. A newer or well-maintained truck burns less fuel per mile. And that’s a direct improvement to your bottom line.

The Bigger Economic Picture

Freight doesn’t move in a vacuum. The broader economic backdrop is cautiously positive, but there are a few things worth watching closely.

Real GDP grew at an annual rate of 2.1% in Q1 2026, according to the U.S. Bureau of Economic Analysis. Unemployment held at 4.3% in May, with non-farm payrolls adding 172,000 jobs, per the Bureau of Labor Statistics. Manufacturing new orders jumped 4.8% in April. Unfilled orders rose in 21 of the last 22 months. That’s a freight demand pipeline that’s still building, not stalling.

On the tonnage side, the ATA For-Hire Truck Tonnage Index fell 2% month-over-month in May to 114.4. But it stayed above year-ago levels for the sixth straight month. Tonnage through the first five months of 2026 is up 2% versus 2025. ATA Chief Economist Bob Costello noted the index is holding up well despite lackluster manufacturing and construction freight.

What the May Data Means for Owner-Operators

The May 2026 data points in one direction: the market is recovering. It’s recovering faster on rates and capacity than on volume. For carriers, that’s good news.

Here’s how we’d summarize the key takeaways:

- Rates are moving your way. Linehaul rates are up nearly 7% year-over-year. Spot rates are climbing even faster. The capacity crunch is holding rates up even without a full volume recovery.

- Fuel is the variable that can eat your upside. Diesel sits at $4.668 per gallon nationally, still above year-ago levels. Route efficiency and equipment health directly impact your margins and fuel efficiency.

- The volume inflection is coming. July 2026 is the projected turning point. Getting positioned before that happens is smarter than scrambling after it.

- Now is a smart time to upgrade or expand. Newer equipment or added trucks could set you up well for the second half of 2026.

We’ve worked with owner-operators and small fleet owners for years. In our experience, the operators who act just before a market turn are the ones who capture the most upside.

How Mission Financial Services Can Help You Take Advantage

The second half of 2026 is shaping up well for carriers with the right equipment in place. Rates are rising. Capacity is tightening. And a volume inflection is on the way.

At Mission Financial Services, we approve applicants in as little as four hours. We also work with credit scores as low as 460. Whether you’re buying your first truck or upgrading your current rig, we have options built for this market.

Apply today and get a decision in as little as four hours.